It is also used to evaluate if a particular activity or service should be performed at the facility or if it should be outsourced to a third-party provider. Conceptually, the contribution margin ratio reveals essential information about a manager’s ability to control costs. The contribution margin may also be expressed as a percentage of sales. When the contribution margin is expressed as a percentage of sales, it is called the contribution margin ratio or profit-volume ratio (P/V ratio). For a quick example to illustrate the concept, suppose there is an e-commerce retailer selling t-shirts online for $25.00 with variable costs of $10.00 per unit. The difference between variable costs and fixed costs is as follows.

Calculating Generated Profit

Alternatively, the company can also try finding ways to improve revenues. However, this strategy could ultimately backfire, and hurt profits if customers are unwilling to pay the higher price. Investors and analysts may also attempt to calculate the contribution margin figure for a company’s blockbuster products. For instance, a beverage company may have 15 different products but the bulk of its profits may come from one specific beverage.

Create a Free Account and Ask Any Financial Question

Knowing how to calculate the contribution margin is an invaluable skill for managers, as using it allows for the easy computation of break-evens and target income sales. This, in turn, can help people make better decisions regarding product & service pricing, product lines, and sales commissions or bonuses. It is the monetary value that each hour worked on a machine contributes to paying fixed costs.

Step-by-Step Guide

For a small business owner, these insights are invaluable in achieving the break-even point and surpassing it towards profitability. On the other hand, variable costs are costs that depend on the amount of goods and services a business produces. The more it produces in a given month, the more raw materials it requires. Likewise, a cafe owner needs things like coffee and pastries to sell to visitors. The more customers she serves, the more food and beverages she must buy. These costs would be included when calculating the contribution margin.

- A key characteristic of the contribution margin is that it remains fixed on a per unit basis irrespective of the number of units manufactured or sold.

- With a contribution margin of $200,000, the company is making enough money to cover its fixed costs of $160,000, with $40,000 left over in profit.

- We may earn a commission when you click on a link or make a purchase through the links on our site.

- Thus, at the 5,000 unit level, there is a profit of $20,000 (2,000 units above break-even point x $10).

- The concept of contribution margin has been central to managerial accounting and financial analysis for decades, providing a straightforward way to evaluate the profitability and efficiency of sales.

This \(\$5\) contribution margin is assumed to first cover fixed costs first and then realized as profit. The contribution margin income statement separates the fixed and variables costs on the face of the income statement. This highlights the margin and helps illustrate where a company’s expenses.

You work it out by dividing your contribution margin by the number of hours worked on any given machine. The contribution margin may also be expressed as fixed costs plus the amount of profit. Thus, the concept of contribution margin is used to determine the minimum price at which you should sell your goods or services to cover its costs. Therefore, it is not advised to continue selling your product if your contribution margin ratio is too low or negative.

Contribution margin calculation is one of the important methods to evaluate, manage, and plan your company’s profitability. Further, the contribution margin formula provides results that help you in taking short-term decisions. For example, assume that the students are going to lease vans from their university’s motor pool to drive to their conference.

Investors often look at contribution margin as part of financial analysis to evaluate the company’s health and velocity. Fixed and variable costs are expenses your company accrues from operating the business. Regularly integrating contribution margin analysis into business reviews is crucial.

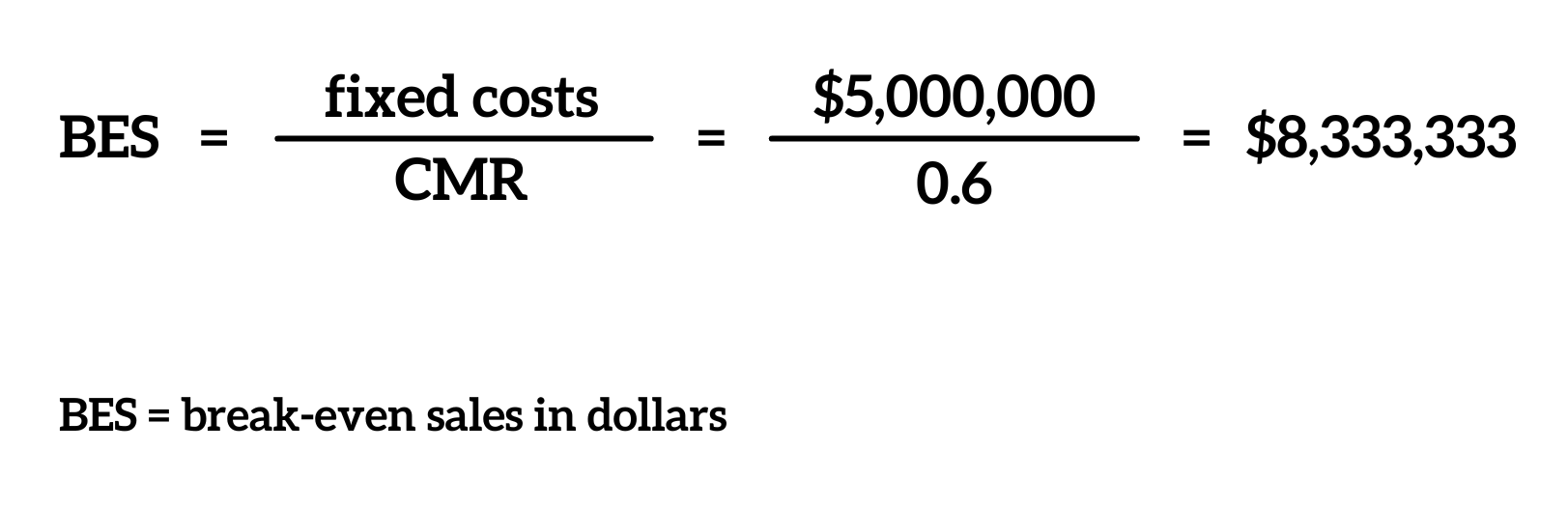

Calculate the total contribution margin ratio by dividing the total of all contributions you calculated in Step 2 by the total sales revenue from Step 1 (you have to have both numbers to calculate this). A business can increase its Contribution Margin Ratio by reducing the cost of goods sold, increasing the selling price of products, or finding ways to reduce fixed costs. A high Contribution Margin Ratio indicates that each sale produces more profit than it did before and that the business will have an easier xero review time making up fixed costs. A low Contribution Margin Ratio, on the other hand, suggests that there may be difficulty in covering fixed costs and making profits due to lower margins on individual sales. In conclusion, we’ll calculate the product’s contribution margin ratio (%) by dividing its contribution margin per unit by its selling price per unit, which returns a ratio of 0.60, or 60%. The contribution margin is affected by the variable costs of producing a product and the product’s selling price.

While contribution margin is expressed in a dollar amount, the contribution margin ratio is the value of a company’s sales minus its variable costs, expressed as a percentage of sales. However, the contribution margin ratio won’t paint a complete picture of overall product or company profitability. Contribution Margin is a critical financial metric that helps business owners understand how much of their sales revenue is available to cover fixed expenses and generate profit. It’s calculated by subtracting variable costs (costs that change with the level of output) from the sales revenue.